5 Steps for CEOs and CFOs to Mitigate the Impact of Tariffs and Economic Uncertainty

Introduction

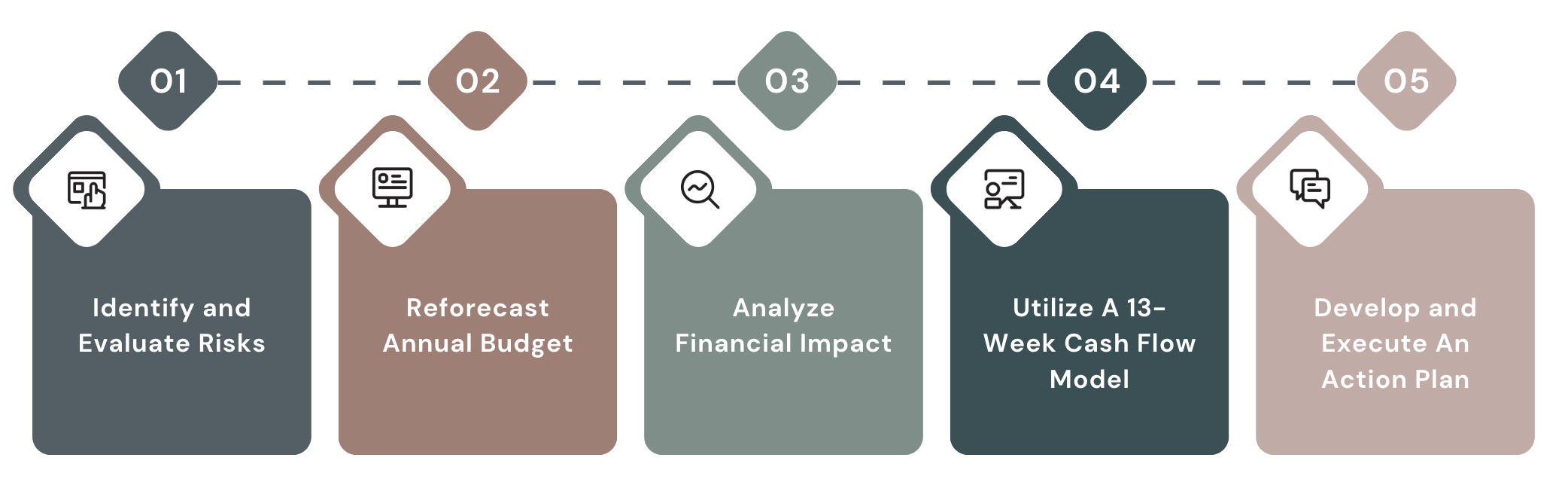

In today's volatile economic landscape, business leaders must proactively identify and manage risks that can threaten profitability, liquidity, and long-term survival. From tariffs to technological disruption and macroeconomic pressures, navigating uncertainty with a proven approach is critical. This post outlines a comprehensive 5-step framework for identifying and evaluating business risks, assessing their impact and likelihood, and developing actionable strategies to ensure financial and operational resilience. The 5 decisive actions every CEO and CFO can take today to position their business for success are:

Identify and Evaluate Risks

Reforecast Annual Budget

Analyze Financial Covenant and Cash Flow Impact

Utilize A 13-Week Cash Flow Model To Monitor Liquidity

Develop and Execute An Action Plan

5 Strategies to Mitigate Tariffs and Economic Uncertainty

Step 1: Identify and Evaluate Risks

Identify Risks for Your Business

Today, businesses are facing a broad range of potential political and macroeconomic risks, including:

Exposure to Tariffs and Trade Restrictions: Businesses that have global supply chains and serve global markets are vulnerable to shifting trade policy and customs regulations. Tariffs could have spillover effects on the economy and consumer demand through inflationary pressure, reducing consumer spending, triggering retaliatory tariffs and boycotts, among others.

Declining Consumer Confidence & Consumer Spending: Rising inflation, increasing household debt, high interest rates, and increasing unemployment can pressure consumer spending, negatively impacting consumer demand for products and services resulting in reduced volume and / or pricing.

Supply Chain Disruption: Geopolitical tensions, pandemics, or logistics constraints can cause product delays, extend delivery timelines, increase raw material and product costs, and increase shipping / freight costs. These changes can reduce profitability and negatively impact cash flow.

Reliance on Immigrant Labor: Changes in immigration policy or labor shortages can disrupt operations and increase costs especially in industries like agriculture, construction, hospitality, and manufacturing.

AI Adoption: The pace of AI development and adoption may leave some firms technologically obsolete or at a competitive disadvantage. Companies that have large technology budgets may be able to capitalize on AI disproportionately and accelerate competitive benefits.

Technological Obsolescence: Rapid technological innovation can erode the relevance of legacy products or platforms and can rapidly change the competitive landscape, eliminate competitive moats, require major investments in new infrastructure to maintain competitiveness, among others.

Capital Markets Volatility: Uncertainty resulting from geopolitical and macroeconomic factors can reduce access to capital and negatively impact the availability and cost of capital for businesses. Banks may tighten lending standards and may be less willing to negotiate on needed waivers or amendments.

Shifting Regulatory Environment: Ensuring compliance with regulations can require both internal and external investment and resources. A shifting regulatory environment requires new policies and procedures, can cause changes in operational processes, supply chains, and other critical systems.

Changing Competitive Environment: Competitors ability to navigate risks impacting your industry and the macroeconomic environment can vary significantly. This can create both competitive threats and opportunities. For example, competitors that are significantly better capitalized during a severe downturn may be less sensitive to changes in revenue and margins and may pursue aggressive pricing / market share growth strategies. Alternatively, competitors that have covenant or liquidity challenges might be open to opportunistic M&A.

Risks will impact each industry and company differently. Before CEOs and CFOs can identify an action plan, they must identify all the potential risks to their business to understand the financial impact and other downstream impacts.

Assess Probability and Timing of Risks

Once risks have been identified, CEOs and CFOs should use macroeconomic and demand trends, historical precedent and qualitative judgment to assess the likelihood and expected timing for each identified risk.

Below is an overly simplified example of potential risks, probability, and timing:

| Illustrative Risk | Probability | Estimated Start | Duration |

|---|---|---|---|

| Impact of Tariffs on Input Costs | 100% | April | 24 months |

| Decline in Consumer Demand | 50% | June | 18 months |

| Increased Competitive Pressure | 50% | June | 18 months |

| Supply Chain Disruption | 75% | May | 9 months |

Assess Severity of the Risks

CEOs and CFOs should quantify the potential impact of these risks on financial statements, including revenue, margins, operating expenses, working capital and capital expenditures. Quantifying the impact is necessary to accurately reforecast the annual budget, evaluate the impact on cash flow and covenants, analyze projected liquidity and develop an action plan.

Below is an overly simplified example of the impact and financial implications of the risks identified above:

| Illustrative Risk | Impact(s) | Current Year Impact | Next Year Impact |

|---|---|---|---|

| Impact of Tariffs on Input Costs | Increase in Product Costs | 15.0% | 5.0% |

| Decline in Consumer Demand | Reduction in Unit Volume | 3.0% | 1.5% |

| Increased Competitive Pressure | Reduction in Pricing | 2.5% | 1.0% |

| Supply Chain Disruption | Increase in Freight Costs | 3.0% | 2.0% |

| Supply Chain Disruption | Increase in Inventory Days to Hedge Against Shipping Delays | 25 days | 15 days |

Step 2: Reforecast Annual Budget

Once the financial risks have been identified, and the probability, timing and severity have been estimated, CEOs and CFOs should reforecast the annual budget. In most cases it is also necessary to review longer-term forecasts to understand the impact of risks on cash flow, financial covenants, and liquidity over the duration of the potential market period of uncertainty. Declining revenue and profitability may be able to be mitigated through proactive steps that are discussed in Step 5 below. Covenant issues and liquidity issues may be able to be mitigated through proactive steps, but could also require accessing additional debt or equity capital, or negotiations with existing lenders and / or investors. A critical output of this reforecasting process is to quantify the size and timing of any potential issues to inform an action plan.

Building A Dynamic Budget

The revised annual budget and longer-range financial model should include a monthly income statement, balance sheet, cash flow statement, debt schedule, covenant calculations and liquidity ratios. It should include clear assumptions for financial, operating, and risk drivers. As market and competitive dynamics change, having clearly defined assumptions will enable faster changes to the reforecast, provide better visibility into future issues, more rapid decision-making, and increase resiliency.

Develop A Probability-Adjusted “Base Case”

The model should be updated with the latest available actual results and should include updated assumptions to reflect the probability adjusted impact of the risks outlined in Step 1 as well as any changes in business performance that have materialized since the original budget was created. This new “base case” forecast should be used to identify the size of any potential financial, cash flow, covenant, and / or liquidity issues and also to inform your action plan (see Step 5). The base case forecast should include detailed assumptions for revenue, cost of goods, operating expenses, non-operating expenses, interest and tax payments, balance sheet and working capital assumptions, capital investments, mandatory debt amortization, debt and equity financing assumptions, among others. Eventually the base case will be updated to incorporate action plans defined in Step 5, but the initial base case should exclude any specific actions to get a clear picture on the scope of any potential issues.

Perform Scenario / What-If Analysis

CEOs and CFOs should include additional scenario analysis as part of the reforecasting process to assist in evaluating the range of possible outcomes, sizing the amount of actions that need to be taken to mitigate issues, and to establish the size of any contingency or reserves.

For detailed best practices for building a dynamic budget model please see our detailed guide or contact the team at Keene Advisors for support.

Step 3: Evaluate Financial Covenant and Cash Flow Impact

Utilizing the reforecasted budget, evaluate revised credit metrics, including financial covenants in existing debt agreements. Key credit metrics are industry specific, but often include:

Debt / EBITDA (earnings before interest, taxes, depreciation and amortization) or Net Debt / EBITDA

EBITDA / Interest Expense

Fixed Charge Coverage Ratio (FCCR)

Debt / Tangible Net Worth

It is important to conform definitions to existing debt agreements. For example, if the credit agreement permits cash-netting, or caps cash-netting those terms should be incorporated into the leverage ratio as part of the reforecasted budget model. As part of the covenant analysis, it is important to define cushion / shortfalls to develop the action plan described in Step 5 and to size the needed mitigation strategies.

“If existing debt agreements permit add-backs for one-time expenses and pro forma adjustments, the financial forecast should include a section to estimate one-time, non-recurring expenses and pro forma adjustments.

Be wary of caps on addbacks and pro forma adjustments that may be included in the debt agreement. Often these caps are based on a percentage of EBITDA. As EBITDA declines the caps can accelerate the decline in EBITDA for covenant calculation purposes.”

In addition to the covenants, the reforecasted budget should evaluate key cash flow and liquidity measures, including:

Working Capital Ratios

Cash Conversion Cycle

Maintenance and Growth Capital Expenditures

Levered Free Cash Flow

Cash + Undrawn Revolver

Current Ratio and Quick Ratio

These ratios will help define the size of any potential issues and inform the action plan to address these issues. For example, if a decline in EBITDA is expected to result in a 5% shortfall on the Debt / EBITDA covenant, then cost savings, revenue initiatives, and debt reduction steps need to close that 5% shortfall. If no amount of changes can address the 5% shortfall in time it may be necessary to negotiate for additional flexibility through waivers or amendments, or to raise outside capital to address the issue. See our CFO’s Guide to Understanding Credit Facilities for more information and strategies.

Step 4: Utilize A 13-Week Cash Flow Model To Monitor Liquidity

A 13-week cash flow model is a short-term cash flow forecast tool that projects a company’s weekly cash inflows and outflows, ending cash, and available liquidity over the next 13 weeks. It is updated weekly, providing a rolling forecast that enables enhanced liquidity planning, improved decision-making, and proactive cash shortfall management. For companies and executives seeking a tool to help navigate economic uncertainty the 13 week cash flow forecast model is essential. The 13-week cash flow model provides a short-term, tactical view of liquidity, enabling companies to:

Ensure sufficient cash availability for operations, payroll, and debt obligations.

Identify potential liquidity risks well in advance.

Optimize working capital by managing receivables, payables, and inventory.

Perform scenario planning by sensitizing timing and amount of cash inflows and outflows.

Support financial decision-making related to capital expenditures, investments, or cost reductions.

Enhance stakeholder confidence (banks, investors, and suppliers) by demonstrating proactive cash management.

The 13-week cash flow model should incorporate the risks identified in Step 1 and the financial impacts forecasted in Step 2. The 13-week cash flow model should also incorporate scenarios to ensure that under a range of potential outcomes the company maintains adequate liquidity at all time.

See our recent post for more information on how to build an effective 13-week cash flow model. Or contact the team Keene Advisors for additional support.

Step 5: Develop and Execute an Action Plan

Once risks have been identified and quantified, potential competitive and strategic impacts evaluated, and the impact on cash flow, financial covenants and liquidity estimated, it is time to develop an action plan. The executive team should evaluate a range of potential mitigation strategies and should quantify the potential benefits, timing and any costs related to the strategy before defining an action plan.

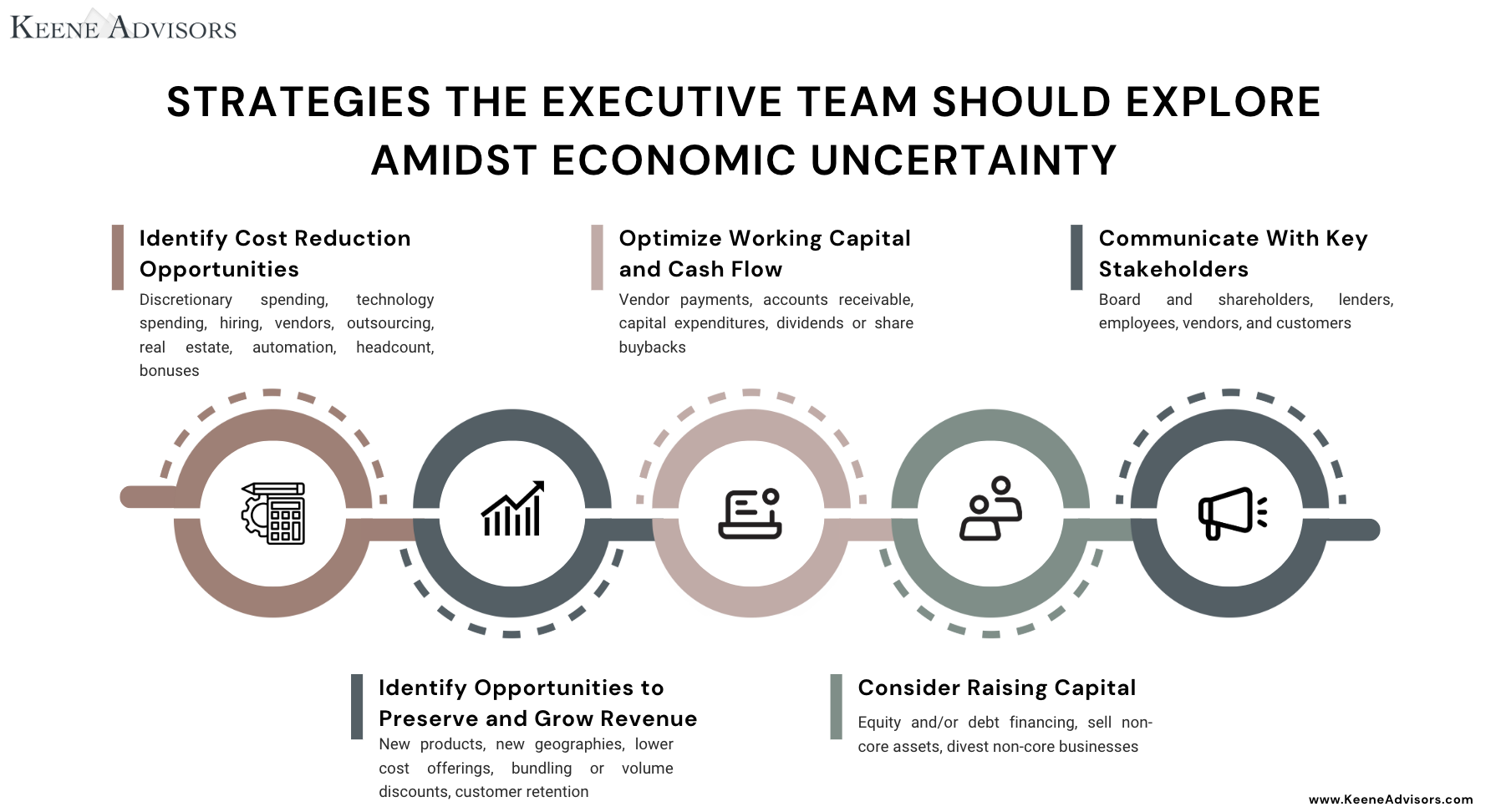

Strategies the Executive Team Should Explore:

Identify Cost Reduction Opportunities

Freeze or reduce discretionary spend (T&E, marketing spend, etc.)

Evaluate technology spend (reduce plan levels, reduce number of seats, eliminate non-core solutions, etc.)

Implement a hiring freeze

Renegotiate vendor contracts

Evaluate outsourcing opportunities

Reduce real estate footprint or sublease unused space

Implement automation and digital transformation to boost productivity

Evaluate headcount reductions and realignment strategies (including costs related to involuntary terminations)

Reduce bonuses or convert cash bonuses to equity to preserve cash flow

Identify Opportunities to Preserve and Grow Revenue

Expand into new products / services, including counter-cyclical segments

Expand operations or sales efforts into new geographies

Pivot to low-cost product offerings

Introduce bundling, loyalty programs, or volume discounts

Invest in customer retention strategies

Optimize Working Capital and Cash Flow

Renegotiate vendor payment terms

Tighten accounts receivable collection efforts

Delay non-essential capital expenditures

Reduce or suspend dividends or share buybacks

Raise Capital, If Needed

Consider raising equity and / or raising additional debt from new or existing investors and lenders

Explore sales of non-core assets or divestitures of non-core businesses

Communicate With Key Stakeholders

Transparency builds confidence and avoids surprises. Develop a tailored strategy for:

Board and Shareholders: Clear articulation of risks and mitigation plans

Lenders: Proactive updates and covenant monitoring

Employees: Honest communication to retain morale

Vendors and Customers: Reassurance of continuity and support

Develop an Action Plan and Assign Accountability

Once potential issues and mitigation strategies have been identified and quantified it is time to develop a specific action plan. Every action plan will be highly customized.

Once the action plan has been defined, a responsible owner and defined timeline should be assigned to every action in order to ensure accountability. Opportunities that provide a near term benefit without negatively impacting long-term growth should be prioritized.

Revisit Reforecast and Scenario Analysis

Once the action plan has been finalized, expected benefits and any associated costs from the action plan should be incorporated into the base case reforecast and scenario analysis. This process can identify unexpected issues and require further iteration on the action plan but is an essential step.

Final Thoughts

Risk is unavoidable, but action is a choice. By proactively identifying threats, quantifying their financial impact, and developing tactical and strategic responses, businesses can emerge more agile and better positioned than their peers. Outstanding leaders will develop an action plan and tackle challenges as early as possible to position for success.

“Risk is unavoidable, but action is a choice...outstanding leaders will develop an action plan.”

Need help identifying and quantifying risks, building a dynamic reforecast, building a 13-week cash flow forecast model, developing an action plan, negotiating with creditors or investors, or sourcing additional liquidity?

Reach out to our expert team of corporate finance and restructuring professionals at Keene Advisors to schedule a complimentary consultation.

About Keene Advisors

Keene Advisors is a Full-Service Strategy Consulting and Investment Banking Advisory firm with experience advising on over $45 billion in M&A, capital raising, and restructuring transactions. Our team has helped clients develop and implement cost savings initiatives, build dynamic budget and 13-week cash flow models, raise capital, navigate lender negotiations, engage with the Board and shareholders on restructuring initiatives.

Securities related services offered through Burch & Company, member FINRA / SIPC. Keene Advisors, Inc. and Burch & Company are not affiliated entities.Keene Advisors, Inc. considers the protection of your information to be a most important priority. View our Privacy Policy for more information.