Leadership Succession and Exit Planning: A Guide for Family-Owned Businesses

Key Takeaways:

Succession planning is a core component of sound governance. Every business will eventually face a leadership transition or an ownership transition that requires foresight and planning. Far too many business owners don’t prepare in advance.

Preserve your legacy, on your terms: Family business owners who plan early have far more options, more leverage, and better outcomes.

Plan for the unexpected: 50% of leadership or ownership transitions are forced by externalities. We recommend starting your succession planning process three to five years before you anticipate a leadership transition or liquidity event.

Leadership and ownership transitions are related but distinct: a leadership transition plan is essential for every business, regardless of whether an ownership exit or business sale is contemplated.

Family-Owned Business Succession Planning

For most business owners, the company they have built represents decades, or even generations, of work and much of their personal net worth. Yet the majority of family business owners have never formalized a plan for what happens to their company when they're ready to step away. In the next decade, an estimated 12 million businesses, representing $10 trillion in assets, will likely change hands, but nearly two-thirds of businesses lack a formal succession plan. According to PwC's 2025 US Family Business Survey, succession planning was a top concern cited by 44% of US family firms.

That risk affects more than just the current business leadership: businesses without a clear plan run the risk of losing customers, missing revenue targets and, ultimately, limiting or completely ceasing operations. That gap is a missed opportunity and a significant continuity risk.

While actively prioritizing the growth of your company, there may not seem to be capacity to plan what happens after retirement, but owners who plan early have far more options, more leverage, and better outcomes.

This guide covers key elements you need to know about both leadership succession and ownership transition planning — from foundational definitions to the most common exit strategies, the advisors you'll need, and how to know when you're ready to start.

What Is Succession Planning?

Succession planning is the process of preparing a company and its owner for a future transition. That transition may involve a change in leadership, a change in ownership, or both. Each requires a different kind of planning.

“Leadership succession planning is a proactive, multi-year strategy that addresses who will run the business, when the leadership transition will occur, and how management authority will be transferred. Exit planning addresses who will own the business, the timing of an ownership change, and the financial and legal mechanics of a sale or transfer of ownership.”

What Is the Difference Between Succession Planning and Exit Planning?

For business owners planning a transition, a leadership succession plan and an exit plan have different focuses.

Leadership succession planning prepares the company for a leadership transition. This can be from a family-founder to a next-generation family member or a non-family leader. An exit plan generally refers to a change in company control or ownership, often as part of a more extensive liquidity event.

Succession and exit planning can occur concurrently. A founder, for example, may transition leadership to a next-generation family member while simultaneously executing a partial liquidity event. But they are often distinct processes with different strategic objectives and different timelines.

The first step is to consciously identify your overall transition goals, your timeline for achieving those goals, and whether those goals ideally include leadership succession planning, an exit or liquidity event, or both.

| Leadership Succession Planning | Ownership Exit Planning |

|---|---|

| Focuses on leadership continuity and long-term stewardship of the business | Focuses on ownership transition, liquidity, and value realization for the owner(s) |

| Addresses who will lead, how leadership authority transfers, and future governance structure | Addresses transaction strategy, valuation, tax optimization, and timing |

| Typically begins well in advance (around 3-5 years) to develop leadership and ensure continuity | Typically begins 2–5 years prior to a liquidity or exit event |

| May involve family members, internal management, or structured ownership transitions (e.g., ESOP) | May involve partial or full sale of the company, recapitalization, or other shareholder liquidity strategies |

| Founder may transition leadership gradually or retain an advisory role while relinquishing day-to-day management authority | Founder may partially or fully step back from ownership; may retain an operational or advisory role during the transition period |

| Often a foundational component of family-owned businesses as leadership is passed from one generation to the next | Often represents the execution of an ownership transfer and value realization strategy |

Why Business Succession Planning Matters to Family Business Owners

For most family business owners, the company is their single largest asset. According to a survey of business owners by Raymond James, nearly half say their business accounts for more than half their wealth, while 90% said it represents at least a quarter of their net worth (Raymond James survey, 2025). That concentration makes comprehensive succession planning inseparable from personal financial planning. Without a defined succession plan, the owner’s wealth remains concentrated, illiquid, and vulnerable to events outside the owner's control.

In an ideal world, owners have ample time to plan for a leadership or ownership transition when they decide to retire or otherwise cease involvement in daily operations. However, research from the Exit Planning Institute shows that nearly 50% of business exits are unplanned. These same events (the “Five Ds”, detailed below) can also force an unplanned leadership transition, even when no ownership change is contemplated. Early succession planning and a clearly defined shareholder liquidity plan can minimize the disruption caused by an unplanned transition.

Who Needs a Leadership Succession or Exit Plan?

Every business owner, even those with owners with no near-term exit intent, still need a leadership succession plan that addresses who will lead the business, and when and how responsibilities will be transferred. Separately, owners interested in an ownership exit should identify how their ownership interest will be valued and sold or monetized.

The following scenarios need a comprehensive plan:

Family-owned businesses with ownership distributed across multiple generations or family members

Companies that may not be family-owned, but where leadership and ownership are concentrated by one person

Businesses with multiple co-owners or partners with diverging long-term goals

Companies with early investors, employee equity holders, or inactive shareholders

Any business owner approaching retirement, or facing a health event or other significant life transition

The Five Ds: Triggers That Force Unplanned Exits

Even the most well-run businesses are not excluded from external forces. Often, one of the following events triggers the need for a succession plan:

Death

Disability

Divorce

Distress (financial or operational)

Disagreement (among shareholders, family members, or other significant stakeholders)

All of these eventualities are mostly outside the business’ control, but establishing a robust succession plan well in advance can significantly increase the likelihood of a favorable transition.

The Unique Challenges of Family-Owned Business Succession Planning

Family-owned businesses face succession planning dynamics that other corporate entities rarely encounter. In a family-owned business, succession considerations may overlap with concerns about family governance or future leadership and/or ownership expectations among family members. Leadership roles may carry emotional significance beyond their economic function and inactive shareholders or family members who own equity but don't work in the business, may have fundamentally different financial goals than active owners.

Key family business succession challenges to address:

Managing the transition of management vs. the transfer of ownership — these don't have to happen simultaneously

Understanding the dynamics of generational succession: less than two-thirds of family businesses survive into the second generation, and only 13% into the third generation (Ward, John, Keeping the Family Business Healthy)

When defining generation leadership and/or ownership succession, confronting "fairness" among children who have different levels of involvement in the business

Preserving company culture and employee relationships through a transition

Avoiding family conflict by surfacing and resolving shareholder disagreements before a transaction begins

Estate planning and personal tax management

Diversification of family wealth

Understanding institutional shareholder liquidity requirements and any change in control provisions

Considering pathways for employee liquidity or employee ownership opportunities

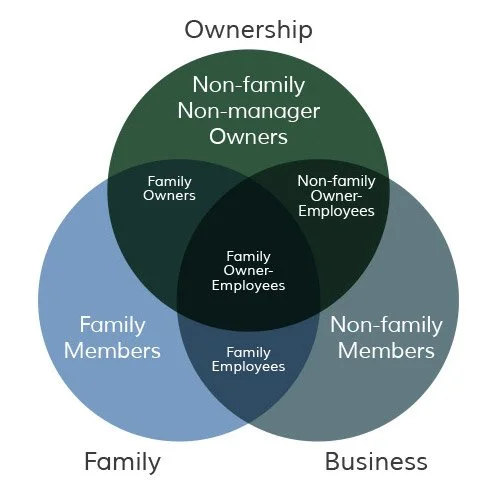

The Three-Circle Model of a Family Business

For many owners, the business is not just a financial asset — it is their source of personal identity, community standing, and generational pride. Owners who treat the financial and emotional components of succession as separate often underestimate how much the emotional complexity can affect decision-making and ultimately the outcome of the leadership succession or exit process. Owners who conflate their personal identity with their business ownership often delay succession and exit planning past the optimal time or valuation window.

This dynamic is well illustrated by the Three-Circle Model of family business systems, which identifies and distinguishes between ownership, management, and family roles. Developed at Harvard Business School by Renato Tagiuri and John Davis, the model highlights how individuals often occupy multiple roles within a family-owned business simultaneously. Each level of ownership and business or family standing comes with distinct priorities, incentives, and emotional drivers. Tension arises when these roles are not clearly defined or consciously managed, reinforcing the importance of addressing both the structural and human dimensions of leadership succession or exit planning. planning.

As part of succession or exit planning, family business owners should consider how each of these categories (ownership, business & family) apply today and how it would change under various succession scenarios.

Exit Planning: The Most Common Ownership Transfer Scenarios for Family-Owned Businesses

Many owners may decide to pursue a partial or full sale or exit from business ownership. There are many possible scenarios, and not all exit strategies carry the same potential outcome. First, the company’s revenue, earnings, assets, industry, and potential valuation will influence the available options. The decision to pursue one type of exit strategy over another should involve an M&A Advisor who can explain the key tradeoffs of each option and help navigate the tax, governance, and legal implications. It’s also helpful to understand the types of M&A acquirers in greater detail.

1. Sale to a Strategic Buyer

Selling to a strategic buyer means a full or partial sale of the business to a company in the same or an adjacent industry. Strategic buyers are typically seeking to expand their addressable market, acquire manufacturing or supply chain capabilities, or reduce the threat of competition. Selling to a strategic buyer is the best option for business owners seeking a full ownership exit and a shareholder liquidity event. Companies with scale, a strong brand, valuable IP, deep customer relationships, or a unique market position are in the best position to pursue a strategic acquisition.

Key Tradeoffs - Strategic

| Considerations | Notes |

|---|---|

| Valuation potential | Often, the highest — strategic buyers may have the willingness to pay a premium valuation for unique synergies of the combined company |

| Control post-close | Typically limited — the acquiring company sets the strategic direction and will often restructure leadership |

| Cultural continuity | Variable — depends heavily on strategic buyer's integration approach |

| Timeline | 6–18 months from process launch to close |

The timeline for a sale to a strategic buyer can vary widely. A well-run sell-side M&A process includes pre-process preparation, marketing, negotiation, due diligence, and regulatory review. More complex transactions, whether in highly regulated industries, or international deals can add considerable time to the sale process.

2. Sale to Private Equity or another Financial Buyer

A sale of majority or significant minority stake to a private equity firm, family office, or other financial buyer may allow the owner(s) to retain partial equity and remaining operationally involved for a period of time in exchange for an infusion of capital in the business and pursuit of a second liquidity event in the future. A private equity firm may consider a leveraged buyout (LBO) to enhance their prospective returns.

A private equity firm or financial buyer has different goals than a strategic buyer, so this route is best for:

Owners who want partial liquidity now while retaining upside in a future transaction, commonly called the "second bite of the apple." A PE firm typically looks to exit 4–7 years after their initial investment, via a sale or IPO

Businesses could benefit from an injection of growth capital, access to operational resources, or guidance from veteran operators in their industry

Thinking About Selling Your Business?

A free guide for business owners

Key Tradeoffs - Private Equity

| Considerations | Notes |

|---|---|

| Liquidity | Partial at close - full value realization typically comes at a future liquidity event |

| Control | Shared governance with PE sponsor - owners retain operational involvement, but reporting and oversight requirements increase with new owners involved |

| Growth capital | Access to institutional capital for expansion, investment, and possibly for acquisitions of other smaller businesses |

| Cultural fit | Critical - PE fund hold periods are typically 4–7 years and their pursuit of operational change may not align with a family-owned business’ stated values or employee makeup |

3. Management Buyout (MBO)

In an MBO, the existing management team purchases the business from the owner(s), typically through a leveraged buyout that may include a combination of debt financing (which can include seller financing), institutional capital, and personal equity.

For businesses that prioritize continuity of leadership, culture, and employee relationships and have a strong management team, MBOs represent a unique opportunity for the management team to play a significant role in the future of the company.

Key Tradeoffs - Management Buyout

| Considerations | Notes |

|---|---|

| Liquidity | Partial at close - full value realization typically comes at a future liquidity event |

| Control | Shared governance with PE sponsor - owners retain operational involvement, but reporting and oversight requirements increase with new owners involved |

| Growth capital | Access to institutional capital for expansion, investment, and possibly for acquisitions of other smaller businesses |

| Cultural fit | Critical - PE fund hold periods are typically 4–7 years and their pursuit of operational change may not align with a family-owned business’ stated values or employee makeup |

4. Employee Stock Ownership Plan (ESOP)

An ESOP (Employee Stock Ownership Plan) is a federally qualified retirement plan that allows employees to gain ownership of the company over time. The ESOP trust purchases shares from the owner, funded through company contributions or debt financing. ESOPs are often structured as partial transactions initially, with the seller receiving proceeds over time as the ESOP trust repays its acquisition debt. The founder may retain a non-ownership operational or advisory role during the transition.

ESOPs may be an ideal option for businesses with a strong, stable workforce and reliable cash flows that value continuity of culture, independence, and increased community impact.

Key Tradeoffs - ESOP

| Considerations | Notes |

|---|---|

| Tax advantages | Potential for significant capital gains deferral (Understanding Section 1042 in ESOP Sales) |

| Valuation | Determined by an independent appraisal under ERISA fiduciary standards. Valuations are typically lower than what a strategic buyer would pay, and that gap can be significant |

| Complexity | Highly structured — requires specialized legal, financial, and ESOP counsel as well as ongoing compliance |

| Transition timeline | Typically 12–24 months from decision to close |

5. Generational / Family Transfer

For family-owned businesses, the transfer of ownership to one or more family members can vary by business. The most popular options are gifting strategies, estate-planning vehicles, structured sales, or a combination of these methods.

This is the best option for companies with a strong desire to remain owned by the family and those with a qualified, willing next-generation leader.

Key Considerations

Unlike selling to a PE fund or strategic acquirer, intergenerational ownership transfers have both personal and business implications to consider:

Gift tax and estate planning implications: The 2026 lifetime gift and estate tax exemption is $15M per individual and $30 million for married couples (IRS.gov, following enactment of the One Big Beautiful Bill Act in July 2025, which permanently eliminated the prior TCJA sunset)

Equalization: How to treat children and other family shareholders who are not active in the business

Management readiness: There’s a difference between owning the business and being able to run it; the business successor must be prepared for a significant management role or be prepared to hire outside of the family

A value gap analysis: Does the business need to grow before a transfer makes financial sense?

Exit Strategy Comparison

| Pathway | Liquidity Level | Control Retained | Primary Type | Best For |

|---|---|---|---|---|

| Strategic Sale | Full | Low | Ownership exit and liquidity realization | Maximizing sale valuation & minimizing future involvement |

| Sale to Private Equity or financial buyer | Partial → Full | Varies | Partial to full ownership exit and partial to full liquidity realization | Accessing a larger pool of potential buyers, raising growth capital, or pursuing a future liquidity event at a higher valuation |

| Management Buyout | Full | None | Exit and leadership succession | Legacy, continuity of company culture |

| ESOP | Transferred over time | Variable | Exit, possible leadership succession | Employee ownership, tax benefits |

| Family Ownership Transfer | Partial or none | High (within the family) | Maintain family ownership | Generational legacy |

Who Helps You Build a Leadership Succession and Exit Plan?

Succession and exit planning should not be a solo project; the legalities and tax implications alone require a level of experience that most family-owned businesses do not retain in-house. Additionally, an external advisor can maintain objectivity and help you identify outside resources and perspectives that can positively influence the planning and decision-making process.

The Right Team of Advisors

The right team includes experienced advisors with a track record of successful client engagements who prioritize the company’s goals within a framework of financial, legal, and governance feasibility.

Advisory Team Responsibilities

| Advisor | Role in Succession and Exit Planning |

|---|---|

| M&A / Investment Banker (Keene Advisors) | Evaluates leadership succession strategies and potential exit opportunities, helps develop an independent or combined strategy that aligns with your goals. Coordinates valuation assessment, prepare for sale process, contacts potential buyers / investors, coordinates leadership succession governance structuring, and manages the extended advisory team |

| Transaction Attorney | Structures legal agreements, reviews representations & warranties, and manages regulatory compliance |

| Tax Advisor / CPA | Optimizes ownership transaction structure for after-tax proceeds, manages estate planning considerations and oversees tax-implications of an ownership transfer |

| Wealth Advisor | Designs a post-liquidity investment and diversification strategy |

| ESOP Specialist | Specialized legal and financial advisory for structuring and executing an ESOP, if applicable |

| Financial Consultant (Keene Advisors) | Strengthens financial reporting, models robust financial projections, and controls financial planning before, during, and possibly after a transition |

Why Start Now? The Case for Early Planning

The most effective planning begins three to five years before business owners anticipate needing it. That may sound very far in advance, but this timeline is not arbitrary. It reflects the typical time needed to:

Clarify whether your goal is a leadership transition, an ownership transition, or both, and sequence your planning accordingly

Address financial reporting gaps and build an auditable track record for your business

Identify and develop internal leadership successors (if applicable)

Resolve shareholder alignment and governance issues

Optimize the value of the business and launch strategic value-creation initiatives

Work through dynamics that are unique to family-owned businesses, including issues that may arise with a generational leadership and/or ownership transfer

In our experience, business owners who start succession and exit planning before a transition is imminent have more options, more leverage, and consistently better outcomes. The best time to start your succession plan is today.

Start Your Succession and Exit Planning Today with an Experienced M&A and Business Strategy Advisor

Since 2015, Keene Advisors has been a trusted partner for family-owned businesses, founders, and growth-oriented middle-market companies, helping them develop and execute customized succession and liquidity strategies aligned with their long-term goals.

If you are beginning to think about leadership continuity, evaluating exit options, or navigating complex shareholder dynamics, contact the Keene team today for a complimentary consultation